Rent vs Buy in Navi Mumbai 2026: What Makes More Financial Sense?

Let us be brutally honest: deciding whether to rent or buy a home in Navi Mumbai is no longer the straightforward choice it was a decade ago. Back then, Navi Mumbai was just a “cheaper alternative” to Mumbai. Today, as we navigate through 2026, it is a premium, globally connected economic powerhouse.

With the Mumbai Trans Harbour Link (Atal Setu) fundamentally changing how we commute, and the Navi Mumbai International Airport (NMIA) redefining the region’s commercial value, property prices have surged. You are now looking at property rates touching ₹25,000 per sq. ft. in Vashi and a rapid 15%–30% appreciation in emerging nodes like Ulwe and Panvel.

So, as a professional or a young family in 2026, do you lock yourself into a 20-year home loan EMI, or do you enjoy the liquidity of renting while investing your capital elsewhere?

This comprehensive guide breaks down the exact financial math, the hidden costs, and the node-by-node reality of the “Rent vs Buy” dilemma in Navi Mumbai.

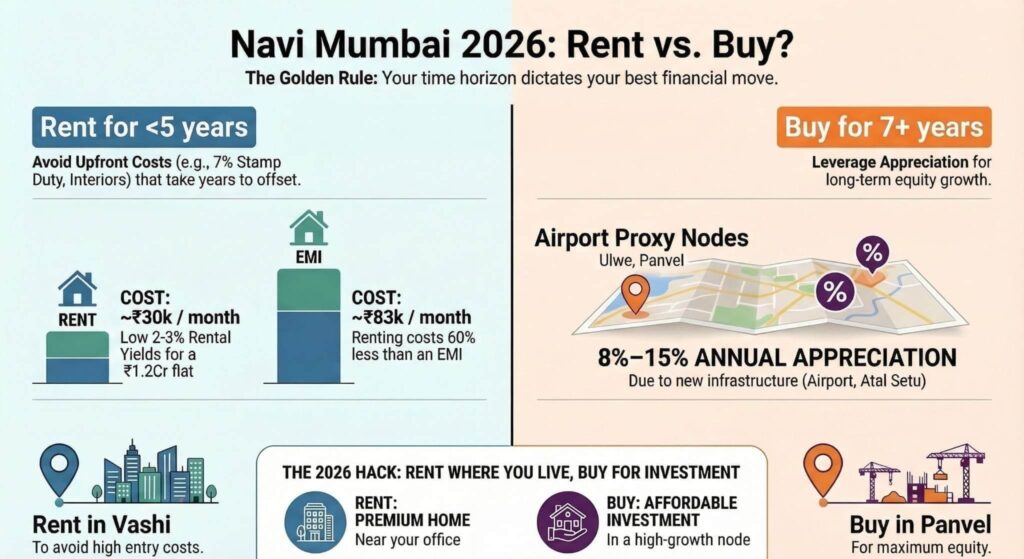

In Navi Mumbai (2026), renting makes more financial sense if you plan to stay in the city for less than 5 years or want to live in premium nodes like Vashi or Nerul, where the rental yield is a low 2%–3%. Buying makes far more financial sense if your time horizon is 7+ years, especially in high-growth corridors like Ulwe, Panvel, and Kharghar, where proximity to the new International Airport and Metro is driving capital appreciation of 8%–15% annually.

The 2026 Navi Mumbai Real Estate Landscape: What Changed?

To make an informed decision, you first need to understand the current playing field. The Navi Mumbai real estate market in 2026 is operating on a completely different frequency than the rest of the Mumbai Metropolitan Region (MMR).

The Three Catalysts of 2026:

- The Atal Setu (MTHL) Effect: The bridge is fully operational, cutting the commute from South Mumbai to Navi Mumbai to under 40 minutes. This has caused a massive influx of Mumbai’s corporate workforce looking for larger, better-planned homes in Navi Mumbai.

- The Airport Reality: The Navi Mumbai International Airport is no longer a “future proposal”; it is an operational reality driving massive commercial and logistics investments into the region. Nodes like Ulwe and Panvel have transitioned from dusty construction zones to premium investment hubs.

- The IT & Corporate Shift: With major IT parks expanding in Airoli, Ghansoli, and Mahape, the localized demand for high-quality housing has skyrocketed.

Because of these factors, the average property price in Navi Mumbai ranges between ₹9,000 and ₹25,000 per sq. ft., depending on the node. Capital appreciation is high, but so is the barrier to entry.

The Financial Math: Renting in Navi Mumbai (2026)

India has historically been a market with very low rental yields, typically hovering around 2% to 3%. This means the annual rent you pay is only about 2% of the total property value. From a pure monthly cash-flow perspective, renting is significantly cheaper than paying an EMI.

The Pros of Renting

- Massive Monthly Savings: If a 2 BHK in Kharghar costs ₹1.2 Crore, your EMI (at 8.5% interest) will be roughly ₹83,000. Renting that exact same flat will cost you around ₹25,000 to ₹35,000 a month. You save nearly ₹50,000 a month in cash flow.

- Opportunity Cost of the Down Payment: To buy that ₹1.2 Crore house, you need to put down at least ₹24 Lakhs (20%). If you rent, you can invest that ₹24 Lakhs into a diversified mutual fund portfolio. Historically, equity markets in India can yield 10%–12% annually, compounding your wealth over time without tying it to a physical asset.

- Zero Maintenance & Taxes: As a tenant, you do not pay the annual NMMC property tax, nor do you bear the cost of major civil repairs, waterproofing, or structural maintenance.

- Ultimate Flexibility: Career moving to Bangalore next year? Just give your landlord a 30-day notice. Renting allows unparalleled geographic mobility.

The Cons of Renting

- The Rent Trap: Rent is a 100% unrecoverable expense. If you pay ₹30,000 a month for 10 years (accounting for a standard 5% annual rent inflation), you will have paid over ₹45 Lakhs to your landlord, and you walk away with zero equity.

- Lack of Stability: In a hot market like Navi Mumbai in 2026, landlords hold the power. You are always at risk of sudden eviction notices or steep rent hikes at the end of your 11-month lease agreement.

- No Customization: You cannot knock down a wall to make an open kitchen. You are living in someone else’s vision of a home.

The Financial Math: Buying a Home in Navi Mumbai (2026)

Homeownership is deeply emotional, but let us look at it purely as an asset class.

The Pros of Buying

- Forced Savings & Equity Building: Every EMI you pay acts as a “forced savings” mechanism. While the interest portion goes to the bank, the principal portion builds your equity. After 20 years, the house is yours.

- Leveraged Appreciation: Real estate is one of the only asset classes where the bank lends you 80% of the money, but you keep 100% of the appreciation. If your ₹1.2 Crore Kharghar flat appreciates by just 6% annually, it will be worth roughly ₹2.1 Crore in 10 years.

- Significant Tax Benefits: The Indian government heavily subsidizes homeownership. In 2026, under Section 24(b), you can deduct up to ₹2 Lakhs of the interest paid on your home loan from your taxable income. Under Section 80C, you can deduct up to ₹1.5 Lakhs of the principal repayment.

- Protection Against Inflation: As the cost of living rises, property values and rents rise with it. A fixed-rate mortgage means your housing cost (EMI) stays the same for decades, while your income grows.

The Cons of Buying

- High Opportunity Cost: Tying up your entire life savings in a down payment makes you illiquid. Real estate cannot be sold overnight if you need emergency cash.

- The “Bank Employee” Syndrome: Taking a heavy loan means a large portion of your monthly income is committed to the bank for the next 15–20 years. This limits your ability to take career risks, start a business, or travel extensively.

- Slower Appreciation in Mature Nodes: While Ulwe and Panvel might see 10%+ growth, mature nodes like Vashi and Sanpada have already peaked. Do not expect your property value to double in 5 years in these established areas.

The 5% Rule: A Quick “Rent vs Buy” Formula

If you hate complex spreadsheets, use the 5% rule to compare the unrecoverable costs of renting versus buying.

Unrecoverable Costs of Buying:

- Property Tax (approx 1% of home value annually).

- Maintenance (approx 1% of home value annually).

- Cost of Capital/Interest (approx 3% — the difference between your mortgage rate and inflation). Total Unrecoverable Cost of Buying = roughly 5% of the property value per year.

The Rule: If you can rent a similar house for less than 5% of its total market value per year, renting makes more financial sense. In Navi Mumbai, rental yields are around 2.5%. By the 5% rule, renting mathematically wins the short-term cash flow battle. However, this rule does not factor in the emotional stability of homeownership or the specific high-appreciation potential of Navi Mumbai’s developing nodes.

Node-by-Node Breakdown: Where to Rent vs Where to Buy?

Navi Mumbai is not a single market. The strategy changes drastically depending on which side of the Sion-Panvel Highway you are on.

1. Vashi & Nerul (The Mature Hubs)

- Average Capital Price: ₹18,000 – ₹25,000+ per sq. ft.

- Average Rent (2 BHK): ₹45,000 – ₹65,000.

- The Verdict: RENT. These are fully developed, highly saturated nodes. Buying a 2 BHK here will cost you upwards of ₹1.8 to ₹2.5 Crores. The capital appreciation has plateaued. If you love the lifestyle, cafes, and infrastructure of Vashi, renting here allows you to live a premium lifestyle without sinking 2 Crores into an asset that will only appreciate at 4%–5% annually.

2. Kharghar (The Balanced Middle)

- Average Capital Price: ₹14,000 – ₹18,000 per sq. ft.

- Average Rent (2 BHK): ₹25,000 – ₹35,000.

- The Verdict: BUY (For End Users). Kharghar is the sweet spot. It has excellent infrastructure (Central Park, Golf Course, Metro), and prices are still reasonable compared to Vashi. It is perfect for end-users who want to buy a home to live in for the next 10–15 years. Capital appreciation will be steady (5%–8%).

3. Ulwe (The Airport Proxy)

- Average Capital Price: ₹9,000 – ₹12,000 per sq. ft.

- Average Rent (2 BHK): ₹15,000 – ₹22,000.

- The Verdict: BUY (For Investors). Ulwe is physically closest to the Navi Mumbai International Airport and the MTHL landing. While the local social infrastructure (malls, fine dining) is still developing, the future upside is massive. If you buy here today, expect significant capital appreciation over the next 5 years as the airport operations scale up.

4. Panvel (The Mega-City Frontier)

- Average Capital Price: ₹8,500 – ₹11,000 per sq. ft.

- Average Rent (2 BHK): ₹12,000 – ₹18,000.

- The Verdict: BUY. Panvel is transforming into a city of its own, dominated by massive integrated townships (like Hiranandani and Wadhwa). It is the most affordable node with excellent railway and expressway connectivity. If you have a budget under ₹80 Lakhs, Panvel is the absolute best place to buy a home in 2026.

The Hidden Costs of Buying vs. Renting

When doing your math, do not just compare EMI to Rent. The “hidden” statutory and operational costs can completely change your budget.

The Hidden Costs of Buying in Navi Mumbai (2026)

- Stamp Duty and Registration: In Maharashtra, Stamp Duty is 7% of the property value (6% for female owners), plus a flat ₹30,000 for registration. On a ₹1 Crore home, that is an instant, unrecoverable cost of ₹7.3 Lakhs.

- GST (Goods and Services Tax): If you buy an under-construction property, you must pay 5% GST. (Ready-to-move-in properties with an Occupancy Certificate are exempt).

- CIDCO Transfer Fees: Since land in Navi Mumbai is leasehold (owned by CIDCO), buying a resale property involves paying a CIDCO transfer fee, which can range from ₹1 Lakh to ₹3 Lakhs.

- Interiors and Furnishing: A bare-shell apartment requires at least ₹10 Lakhs to ₹15 Lakhs for basic modular kitchens, wardrobes, and false ceilings.

The Hidden Costs of Renting

- Heavy Security Deposits: Landlords in Navi Mumbai typically demand 3 to 6 months of rent upfront as a deposit. For a premium flat, this can mean locking up ₹2 Lakhs in cash that earns zero interest.

- Brokerage Fees: Every time you move, you pay 1 month’s rent as a brokerage fee. If you move every 2 years, this becomes a significant recurring expense.

- Shifting and Moving Costs: Hiring professional packers and movers locally in Navi Mumbai costs ₹8,000 to ₹15,000 per move.

Emotional vs. Financial ROI: The Intangibles

Spreadsheets are logical; human beings are not. The Rent vs Buy debate often comes down to emotional ROI.

The Case for Buying (Stability): If you have children, stability is paramount. You want them to go to the same school without the fear of being uprooted because a landlord decided to sell the flat. Homeownership provides a psychological anchor. You can drill holes in the wall, adopt a pet, and build a lasting relationship with your community.

The Case for Renting (Freedom): The modern workforce is highly mobile. If you are in your 20s or 30s, your career might demand you move to Hyderabad, Dubai, or Singapore in a few years. Buying a house ties you down. Renting allows you to upgrade your lifestyle immediately—you can rent a luxury apartment with a sea view in Seawoods for ₹60,000 a month, whereas buying that same apartment would require an EMI of ₹2.5 Lakhs.

Final Verdict: What Makes More Financial Sense in 2026?

So, what is the final answer for Navi Mumbai in 2026? It all boils down to your Time Horizon.

- The 1 to 5 Year Horizon = RENT. If you are unsure where you will be living in 5 years, do not buy. The upfront costs of buying (Stamp Duty, Registration, GST, Interiors) are too high to recover in a short timeframe. Rent, enjoy the lifestyle, and invest your surplus cash in equity markets.

- The 7+ Year Horizon = BUY. If you are settled in your career, your family is rooted in Navi Mumbai, and you plan to stay for at least 7 to 10 years, buying is mathematically superior. The Navi Mumbai International Airport, the Atal Setu, and the expanding Metro network ensure that property values will continue to appreciate steadily. Every EMI you pay builds equity in one of India’s fastest-growing real estate markets.

The Ultimate Hack for 2026: If you want the best of both worlds, practice “Rent Where You Live, Buy What You Can Afford.” Rent a comfortable house near your office in a premium node like Vashi to save on commute time and EMIs. Simultaneously, buy a smaller, affordable property in a high-growth node like Panvel or Taloja as an investment to build equity and generate rental income.

FAQ’s

1. Is it a good time to buy property in Navi Mumbai in 2026?

Yes, 2026 is an excellent time to buy property in Navi Mumbai if your investment horizon is long-term (7+ years). The operationalization of the Mumbai Trans Harbour Link (Atal Setu) and the progress of the Navi Mumbai International Airport are driving steady capital appreciation, particularly in nodes like Ulwe, Panvel, and Kharghar.

2. Which is better for investment in Navi Mumbai: Kharghar or Ulwe?

For pure investment and high capital appreciation, Ulwe is currently superior due to its immediate proximity to the new International Airport and the Atal Setu landing. However, for end-users seeking immediate lifestyle amenities, schools, and parks, Kharghar remains the more balanced and established choice.

3. What is the average rental yield in Navi Mumbai?

The average rental yield for residential properties in Navi Mumbai in 2026 typically ranges between 2% to 3.5%. This means if you buy a property worth ₹1 Crore, you can expect an annual rental income of roughly ₹2 Lakhs to ₹3.5 Lakhs before taxes and maintenance.

4. Will property prices fall in Navi Mumbai?

No significant price drop is expected in Navi Mumbai in the near future. High demand driven by corporate migration, combined with limited land supply and massive ongoing infrastructure projects, supports strong price stability and gradual appreciation across the region.

5. What are the hidden costs of buying a flat in Maharashtra? When buying a flat in Maharashtra, budget an additional 10% to 15% over the property price for hidden costs. These include Stamp Duty (7%), Registration Fees (₹30,000), GST for under-construction properties (1% to 5%), CIDCO transfer charges (for resale in Navi Mumbai), and interior furnishing costs.